Like many, I cannot recall when FinTech became a thing, but I am reliably informed that the word was conceived in 1971. The concept is not as new as some perceive it to be, and that is because the evolution of FinTechs and the role they play in finance, has developed slowly and silently. To understand the role they play in the banking future, it is necessary to first go back and see how these mini organisations have driven value historically.

I have grown up in an era that has seen banking move from analogue to digital, and from banking to Fintech, and it has been a painful journey for all involved. I remember when I first wrote a paper on adoption of internet payments in the 90’s, and the role they would play in making shopping easier, it was laughed off quickly. I had several senior banking mentors telling me that whole thing of buying things on the net would never take off.

A lot has happened since the 90’s when internet-enabled living first became mainstream, and many banking professionals talk about various iterations of the FinTech market namely 2.0, 3.0 etc. I prefer to see these iterations as industry seasons, as nothing really lasts forever, and eventually everything comes back into fashion with some modifications. For me we have seen 4 Fintech seasons thus far, and each season has been “binge-watch” worthy…

- Season 1: Moving across the water. The ability to send funds across the Atlantic in the late 1800’s was a game changer for both banking and for consumers. The establishing of the infrastructure to enable this is well recognised as the catalyst for electronic fund transfer and payments. This is the first brick in the fintech wall

- Season 2: Your flexible friend the credit card. This is where several of the mainstream and non-mainstream providers such as Diners and American Express were able to provide consumers with the first taste of deferring payment without taking out a loan

- Season 3: Birth of Electronic Banking. Rapid progress is made off the back of investments made in Season 2, where there is another key milestone in the form of the launch of the ATM. In this season we also see the arrival of SWIFT and significant movement towards electronic banking for personal as well as business customers

- Season 4: Episode 1: Revenge on the 2008 Megalomaniac Banker. This is perhaps the most pivotal period in the history of the FinTech, where the overall level of dissatisfaction, and anger over the banking crisis, spurned many entrepreneurs into action. These individuals set about identifying parts of banking that they thought were broken and came up with lean ideas to fix them. Enter FinTech’s like PayPal (1998), Envestnet (1999), Xoom (2001) and Zopa (2005)

- Season 4 : Episode 2: The UI/UX Wars. Following the success of Episode 1, another wave of innovation followed where more parts of the banking value chain such as lending, managing money, and making payments were being re-imagined by new start-ups. We enter the era of seeing at least one new FinTech being born daily. However, challenges to solve for remain broadly static. We now have industry clutter where we have a lot of organisations, by that I mean a lot, looking to solve for the same problem in broadly the same way, just with different UI/UX

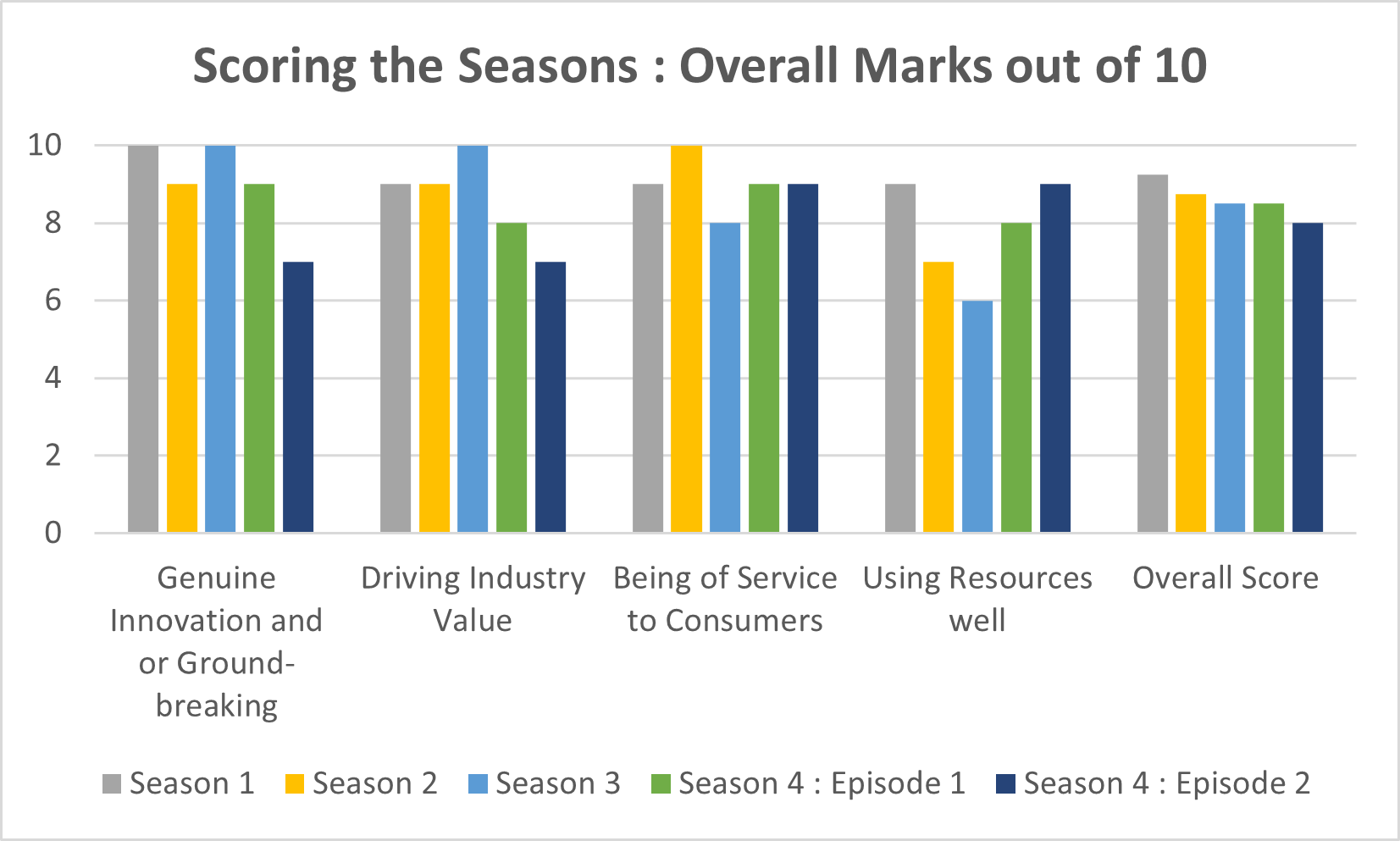

If I were to reflect on each of the Seasons, and think about how I would rate them for being genuinely innovative, driving industry value, being of service to consumers and using resources sensibly it would look like something like this

Driving Innovation & Value: Season Scores out of 10

Please note these ratings are my own personal subjective perspective and are not attributed to any organisation I work with currently or have worked with historically. Disclaimer done!

This perspective shows that over time innovation has become less and less original, and at best has kept pace with overall improvements in technology. The ability to drive industry level progression has also been limited and is perhaps more incremental improvement than transformational; a thousand little improvements does not equate to a gamechanger. Additionally, the overall value to consumers is potentially less obvious with these point-solutions that don’t always take into account someone’s overall financial position.

The market has become cluttered with FinTechs, the majority of which fail to scale because it is not clear which part of the value agenda that they are catering for, and they do not have the brand presence to muddle along. In the absence of driving value survival is a challenge. There is a higher prevalence of copying ideas from others and trying to solve for the same challenges in the same way, but with a difference look and feel. This is perhaps not the best use of talents, skills, and resources.

Winning in this environment, especially against the backdrop of Open Banking and COVID fuelled digital acceleration, needs a new FinTech formula.

So, what is the takeaway for somebody wanting to play a major role in Season 4: Episode 3?

- Be clear on the segment you are looking to serve, and why!

- The world is cluttered so why are you different, make sure that this is firmly answered

- Have clarity on the value proposition to the target segment; it cannot be just about a more attractive design

- Think about propositions as a collection of features which make life easy, and genuinely make a difference to the way in which finances can be managed

- Think industry wide issues which can be solved, and that incumbents can use to drive effectiveness and better customer experience easily

- Partner with other FinTechs where viable as this helps to alleviate the burden on an already creaking planet, and shrinking pool of available talent

- Lastly, not all Bankers are muppets, so remember when engaging with the industry players, it maybe your first rodeo, it certainly will not be theirs. Be respectful as there have been many seasons before you, and many seasons and episodes will follow

The last point is key, as history shows many, not all, successful FinTech’s will end up having extremely healthy partnerships with traditional banks. This is a key part of the model, and a key element of driving sustainable value.

The next few blogs will focus on broadening out the themes above for specific banking domains inorder to give further insights and perspectives.