A lot being is being documented on how COVID has accelerated the digital banking and transformation agenda, as more remote channels have become the norm for everyday banking. Similarly, the pandemic has also had a very profound effect on payments, and ironically it is the way in which cash is used that is driving how future trends will shape up.

For several decades banking pundits have been predicting the demise of cash, and yet pre pandemic the use of cash, despite its declining usage, was still very much in circulation. Data from Statista shows that 50.5% of transactions undertaken by consumers in 2000 were cash, in comparison to 14.6% in 2019, down but definitely not out.

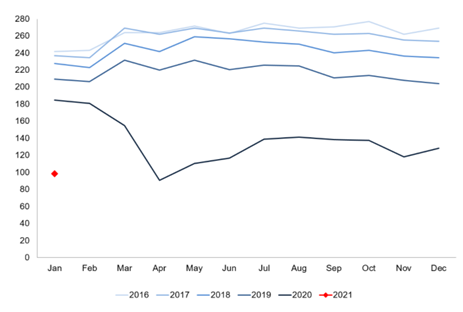

If we use data from LINK as a proxy for cash usage in the UK and compare the week-on-week cash withdrawal trends from ATMs across the LINK network, further evidence is shown on the continuing decline of cash-based transactions. The latest LINK data shows a c. 48% decline in cash withdrawals looking at YTD 2021 versus the same period last year (see table below for trends).

LINK Transaction Volumes (millions) – Source : LINK Statistics & Trends (These figures only show transactions and balance enquires at LINK ATMS, but do not include transactions made by customers at their own banks’ or building societies’ ATMs)

Despite the crisis, and the significant move to contactless payments, as well as the shift from physical store spend to online spend, payment systems have shown remarkable resilience with no reported outages. Most banks and retailers have stepped up during this period, and gone the extra mile to support consumers as they navigate the challenges bought about the pandemic e.g. mortgage payment holidays, bounce-back loans, extending refund windows for purchases, more click & collect options etc. It is also fair to say that with or without the hygiene, or health and safety angle of handling physical notes and coins, cash use is on the decline, and is expected to decline further.

Despite the crisis, and the significant move to contactless payments, as well as the shift from physical store spend to online spend, payment systems have shown remarkable resilience with no reported outages. Most banks and retailers have stepped up during this period, and gone the extra mile to support consumers as they navigate the challenges bought about the pandemic e.g. mortgage payment holidays, bounce-back loans, extending refund windows for purchases, more click & collect options etc. It is also fair to say that with or without the hygiene, or health and safety angle of handling physical notes and coins, cash use is on the decline, and is expected to decline further.

This pattern however does not mean that overall transactions are declining, it is just reflective of these transactions migrating to other payment methods such as debit cards, or contactless payments. The overall move to digital payments is favourable, however the banking industry has not really geared up for such a significant unplanned re-pivot. There are many commercial considerations that need to be worked through as these micropayments (average transaction value of c. £12.00), grow in scale and velocity.

The economic P&L impact for banks as these micropayments grow in volume is challenging, as the cost effectiveness of processing, clearing, and settling these transactions is lower on a fully absorbed basis. This is against the backdrop of significant legacy technology estates that must now deal with a significant number of high-velocity, and lower value transactions that need to be fulfilled real-time. To help understand what determine payments profitability, there are a few levers that come into play:

- Net interest income which is under significant pressure globally accounts for c. 60% of payment revenues

- For card-based transactions there are interchange fees payable by payment processor to providers that issue those cards

- Retailers pay for accepting card payments in the form of a merchant service charge (MSC), and these have been declining over the last two decades as interchange rates have dropped, causing pressure on payment processor revenue

- Network fees that are paid to route, clear and settle transactions

- Infrastructure costs for traditional players tend to be higher, as legacy architecture is expensive to change and harder to remain compliant especially when providing faster, real-time payments

- International, FX and cross-border fees are also applicable for non-domestic payments

- Open Banking payments, that is direct from account payments, are more economic challengers for card-based payments, but do not currently offer the same payment protections

Looking at the levers above, how should payment providers and processors think about responding to these trends? Pressure mounts to eradicate cash quicker, high-cost payments operating models make the economic case harder to prove over the long term, and changes in consumer spending call out for different approaches to cater for more micropayments.

Four areas are explored to give some ideas on how to improve the overall value from payments:

- Offer a “broader-than-payments” play – an option that can be considered for b2b payments, or the SME banking model. Concept is to provide an overall composite financial management service for a amalgamated fee. Services like payment acceptance, overdrafts, deposits, loans, deferred settlement, or factoring can serve as ways to support the overall cash flow of an SME business. All of these “transactions” can be managed across the most cost-effective channel for the bank, yielding in a win-win situation for both the consumer/SME and the bank

- Technology & Infrastructure – Transformation of overall payments infrastructure to support lower cost models is a necessary step if any provider is looking to stay in the game. Micropayments are a scale play as the margins on these smaller value transactions are skinny, which means you need a lot more of them against a much lower cost base. Traditionally, for payment business embedded in a bank, c. 70% of budgets on an annual basis have been used just to stay compliant and manage regulatory change. Investment dollars for more discretionary and future-centric spend has always been challenged. The ability to be compliant, resilient, secure, and innovative to stay ahead of the game can only be achieved if the underlying technology estate is nimble and agile. This is a critical component of being able to compete effectively and strategically

- Leveraging Data in exchange for Value – Examination of a larger data play to augment payment economics or drive more value from a single transaction irrespective of value. The options to drive incremental revenue form seeing all this rich data on purchasing patterns and behaviour can include:

- Creation of new underwriting models that look at consumer/business spending patterns, areas of spending, and responses to economic events, as potential indicators of creditworthiness. Additionally, examination of how newer forms of real-time fraud management could work with real-time transaction information being available

- Launching of loyalty schemes that can work across an industry sector as opposed to a single retailer e.g., Tesco Club Card v UK Grocery Loyalty. This helps to stimulate a further switch from cash to more convenient payment methods (cards, wallets, Apple Pay, Google Pay etc), as well as driving value to end consumers in the form of easy redeemable points

- Development of new financial management tools to help individuals manage their money or cashflow more effectively. Allowing spend to be reverse engineered to the most cost-effective method/channel post event. This is a real value add as it allows a meaningful retrospective to be applied to financial decision making which does not take the form of “if you had done this then you could have saved…”, it course corrects for suboptimal decisions and tangibly helps consumers

- Customer-centric to Hygiene-Centric Payment models. As concerns around viruses and contamination persist, more and more mechanisms for transitioning towards becoming more touch-less in the broader sense, are needed. Shifting the POS based contactless limits from £30.00 to £45.00 was a sensible move, but what happens after £45.00? so a key design feature of any payment acceptance method going forward should be more hygiene-centric, as even things like fingerprint/facial recognition become challenged because of gloves/facemasks. Not so much a gimmick as a potential necessity as the world becomes increasingly aware of the significant damage a pandemic can create in a short period of time

In conclusion, there are several elements that need to be addressed to manage profitability as payment trends move and shift in response to many macroeconomic factors, health & safety, and further swings in consumer purchasing preferences. There is perhaps a larger burning platform here, in that for any payments business to be viable in the post COVID era, with the expected economic downturn, it needs to have skinny-tech-ops. The trends around cash usage decline, and the need to be able to prepare for more micropayments, indicate that lower-cost business models are needed to make operating in this space commercially viable.

We should note that some of the larger payment players are embedded in traditional clunky banks, where becoming a lower-cost model is a challenge – cost allocations are an internal organisational tax that kill profitability for these businesses. This does then really open the pandoras box debate around whether it is better for any payments model to operate standalone if it is to have the chance of being profitable and innovating at pace. I do ponder if banks like HSBC and RBS/NatWest had early awareness of how challenging driving EBITDA in a payments business would become, and in hindsight were smart divesting their retail payments, or merchant acquiring businesses several years ago…