In the main, people find managing their finances challenging, and the process of setting out a budget, to help manage income and outgoings, do not always help in the long run. Yet when people are struggling with understanding how they can manage their money better, going to their bank does not appear to be the obvious choice!

Most consumers need support to understand how to reduce bills, whether that is utility bills, car insurance, consolidating loans, finding cheaper alternative for mobile airtime, credit cards etc. In this scenario more proactivity is needed by banks, which stretches more broadly than sharing an account statement on a mobile app, which shows payments already undertaken. Some of the newer digital banks have made some attempts to apply simple techniques for extrapolating a customer’s available balance at the end of the month. Using historic data to map regular payments, direct debits and standing orders and estimates for discretionary spend, a projected month end balance is predicted. None of these techniques are proactive when it comes to helping reduce overall outgoings, as at best, they help to establish what has already past, which obviously cannot be changed or reversed.

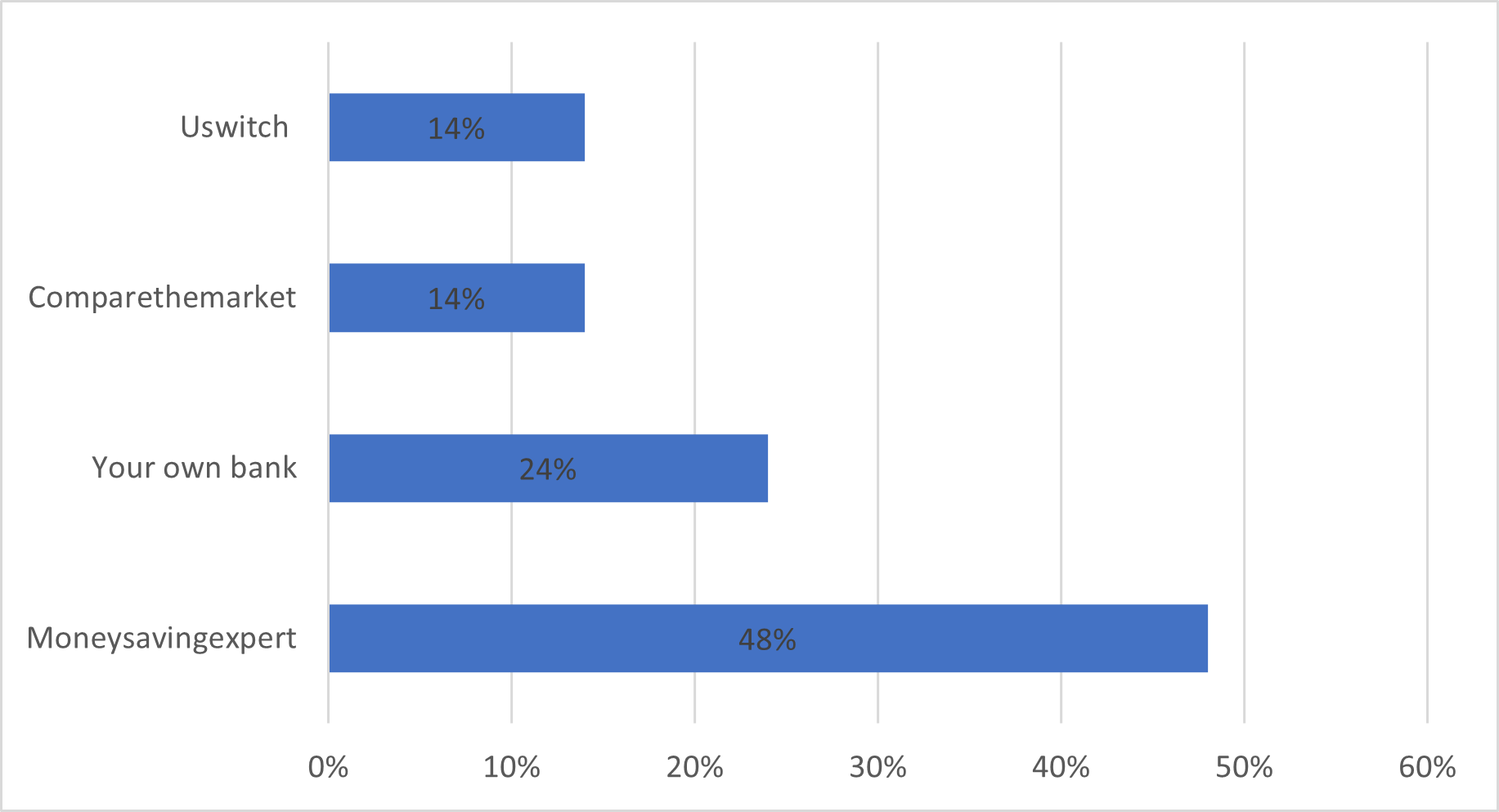

This is the main reason why providers like moneysavingexpert, comparethemarket.com, Uswitch exist; they aim to make life easier for consumers, by searching out the best available ways in which money can be saved. Quite often these providers offer sensible advice on how to manage bills, in a simple and easy to understand manner, and make it easy to switch providers when better deals are found. I ran a quick temperature check poll on Twitter last week, the question posed was “when looking for advice and tips on how to reduce your financial outgoings, where do you go first” The results were as follow:

This survey was not designed to be a broad comprehensive study, but a quick moment in time yardstick to gauge a high level view from a handful of people who voted. The poll sparked a lot of debate among my colleagues, and in summary none of us were really surprised that people in the main, would not see their bank as the primary place to get advice on managing household bills and budgets.

Banks could learn from these comparison service providers, especially when it comes to thinking about supporting customer financial well-being. Here, three ideas are explored to establish how traditional banks can be more front of mind, when consumers are trying to avoid financial hardship, looking to economise, and can in turn support these customers from the mental health impact of continual financial stress:

- Allowing customers to create more of a pen portrait of their overall style of living to help improve finances. Capturing information with the aim of proactively helping to reduce expenditure. Examples could include:

- Size of home and energy usage to help scan the market for better deals on fuel

- Assessing how many people are in the family, and what their interests are to examine deals that may help save money on things like streaming services

- Examine options for running a family vehicle more efficiently, from car insurance to the type of financing agreement

- If renting, having a look at more cost-effective rental options in case a move is on the cards, or even a property purchase

- Bringing day-to-day money saving tips into banking interactions through working with several of the providers mentioned above, where customers would naturally go for help with economising. Creating these tie-ups helps to aggregate more financial data, hence making the ability to search for advice and discounts easier. This also helps the consumers to create a space for managing the household budget more dynamically, as there are always checks being made in the background, to see if they are on the best deal for everyday spending, and significant bills. Additionally, this could also help customers find greener or sustainability-centric suppliers at the same time, if this is something that factors into the decision-making process, when thinking of switching provider

- More widely we see several schemes in play in the b2b space, where banks work with providers like the Federation of Small Businesses (FSB) to help bring deals together for smaller customers. These SMEs can then access pricing plans that are based on “clubbing together” transactions to achieve a better discount, akin to the scale discounts available for large customers. The same approach could be adopted for consumers, where the banks could work with utility providers, mobile phone services providers, streaming services, and others to secure discounts for their own customer base

In conclusion, if a bank is not seen as the immediate go to place, to get help with managing finances, then some rethinking is in order. Quite often patterns of spending, and clever data visualisation techniques, are not enough to help consumers when it comes to reducing their outgoings. These money management tools may help with discretionary spend but does not always proactively help with reducing everyday bills, and here is an opportunity for banks to step up. If banks can use their purchasing power to bring economies of scale to either consumers, or SMEs, that surely has got to be a win-win situation, especially as we enter into a challenging climate, with all feeling the effects of the pandemic.